In the digital age, technology continues to evolve and reshape industries around the globe. Blockchain Technology is one of the most exciting and impactful innovations in the past decade. You may have heard of it in connection with cryptocurrencies like Bitcoin, but Blockchain is much more than just the backbone of digital currencies. It’s a technology with the potential to transform industries, enhance transparency, and create new opportunities for businesses and individuals alike. This article explores what Blockchain is, how it works, its applications, benefits, challenges, and its potential future.

What Is Blockchain?

At its simplest, Blockchain is a digital ledger or database that records information securely, transparently, and tamper-proof. Unlike traditional databases managed by a central authority, Blockchain operates on a decentralized computer network, often called nodes. This decentralization is one of the key features that makes Blockchain so powerful.

Each block in a blockchain contains a list of transactions, a timestamp, and a reference to the previous block, creating a chain of information. This structure ensures that once data is recorded on the Blockchain, it cannot be altered without consensus from the entire network.

How Does Blockchain Work?

Understanding Blockchain starts with breaking down its key components and processes:

Blocks

Blocks are the fundamental building units of a blockchain. Each block contains data, such as transaction details, timestamps, and a reference to the previous block’s unique identifier called a hash. This hash acts as a digital fingerprint, ensuring the block’s content remains unchanged. If someone attempts to alter the data in a block, the hash changes, breaking the chain’s structure. This makes the blockchain tamper-proof and ensures the integrity of the information.

Nodes

Nodes are individual computers connected to the blockchain network. They perform essential tasks such as validating transactions, maintaining a copy of the Blockchain, and ensuring that all copies are synchronized. Nodes work together to create a decentralized system, reducing reliance on a single authority. This decentralization makes the Blockchain more secure because no single entity can control the entire network. For instance, if a node is compromised, other nodes in the network will still have accurate copies of the Blockchain.

Consensus Mechanisms

Adding a new block to the Blockchain requires agreement among the network’s participants. This agreement is achieved through consensus mechanisms. Two widely used mechanisms are:

- Proof of Work (PoW): In this method, nodes (called miners) solve complex mathematical problems to validate transactions and create new blocks. This process requires significant computational power and energy, which deters malicious activity. Bitcoin uses PoW.

- Proof of Stake (PoS): Instead of solving mathematical problems, validators in PoS are chosen based on the number of coins they hold and are willing to “stake” as collateral. This method is more energy-efficient and is commonly used in newer blockchain systems like Ethereum 2.0.

These mechanisms ensure that only valid transactions are added to the Blockchain and prevent fraudulent activities.

Decentralization

One of the defining features of Blockchain is its decentralized nature. Unlike traditional systems managed by a central authority, Blockchain operates across a distributed network of nodes. Each participant has equal rights and access to the network. Decentralization makes the system more transparent and resilient. It also removes the need for intermediaries, which can reduce costs and increase efficiency.

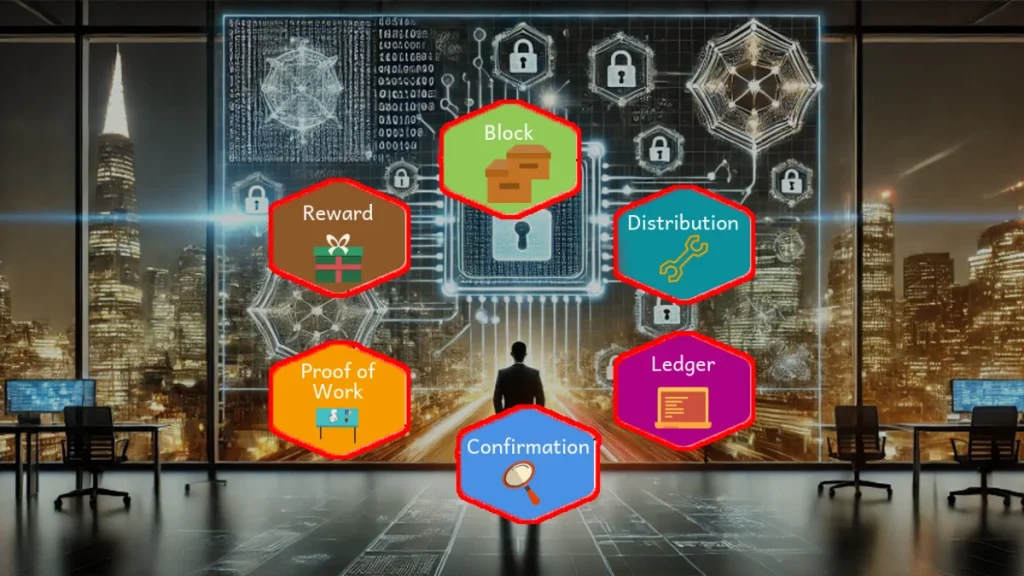

Example of a Blockchain Transaction

To understand how Blockchain works in practice, consider a cryptocurrency transaction. Suppose Person A wants to send Bitcoin to Person B:

- Initiation: Person A creates a transaction request, specifying the amount of Bitcoin to be sent and Person B’s wallet address. This request is broadcast to the blockchain network.

- Validation: The nodes in the network validate the transaction by checking whether Person A has sufficient funds and ensuring that the transaction details comply with network rules.

- Block Creation: The transaction is bundled into a new block once validated.

- Consensus: The network’s nodes agree to approve the new block using mechanisms like PoW or PoS.

- Recording: The approved block is added to the Blockchain, creating a permanent and unalterable transaction record.

- Confirmation: Person B receives the Bitcoin, and the transaction is completed.

This process ensures that the transaction is secure, transparent, and immutable, which are the core benefits of blockchain technology.

Types of Blockchains

There are several types of blockchains, each suited for different purposes:

Public Blockchains

Public blockchains are open networks that anyone can join. They are fully decentralized and do not rely on any central authority. Anyone with internet access can participate as a node, view transactions, and contribute to the network’s security and operation. These blockchains use consensus mechanisms like Proof of Work (PoW) or Proof of Stake (PoS) to validate transactions and add new blocks.

Examples of public blockchains include Bitcoin and Ethereum. Bitcoin was the first Blockchain and is primarily used to transfer digital currency. On the other hand, Ethereum is designed to support smart contracts and decentralized applications (dApps), making it more versatile.

Public blockchains are ideal for projects that prioritize transparency and accessibility. However, they can face scalability challenges due to the high volume of participants and transactions.

Private Blockchains

Private blockchains are restricted networks where only authorized participants can access and contribute. These blockchains are controlled by a single organization or entity, making them centralized compared to public blockchains. Businesses often use private blockchains for internal operations, such as tracking supply chains or managing financial transactions.

Because they are closed systems, private blockchains offer greater control and efficiency. Transactions are faster, and scalability issues are minimized since fewer participants are involved. However, this comes at the cost of reduced transparency and decentralization.

Examples of private blockchains include Hyperledger and Corda. These platforms are tailored for enterprise use, providing the necessary tools for businesses to build their blockchain solutions.

Consortium Blockchains

Consortium blockchains are semi-decentralized and controlled by a group of organizations rather than a single entity. They are designed for industries that require collaboration and data sharing among multiple parties, such as banking, healthcare, and supply chain management.

In a consortium blockchain, only selected participants can access and validate transactions. This setup ensures all parties maintain trust and transparency while protecting sensitive information.

An example of a consortium blockchain is the IBM Food Trust, which companies like Walmart and Nestlé use to trace the origins and movement of food products. These organizations can improve efficiency and accountability across the supply chain by sharing data on a single platform.

Hybrid Blockchains

Hybrid blockchains combine the features of both public and private blockchains to provide greater flexibility. In a hybrid system, some parts of the Blockchain are open and accessible to the public, while others are restricted to authorized participants. This approach allows organizations to balance transparency and privacy based on their needs.

For instance, a company could use a hybrid blockchain to make general information about its operations available publicly while keeping sensitive financial data private. This combination is particularly useful for businesses that must comply with regulatory requirements while maintaining a degree of openness.

An example of a hybrid blockchain is the Dragonchain platform, which offers customizable solutions for businesses. Hybrid blockchains are becoming increasingly popular as they cater to diverse use cases and offer the best of both worlds.

Applications of Blockchain

Blockchain technology has found applications in various industries beyond cryptocurrencies. Let’s explore some of its most notable uses:

Finance and Banking

Blockchain has revolutionized the finance and banking sector by providing a faster, more secure, and cost-effective way to manage transactions. Traditional banking systems often rely on intermediaries like clearinghouses, which can slow down processes and increase costs. These intermediaries are removed with Blockchain, allowing peer-to-peer transactions to settle almost instantly. Decentralized Finance (DeFi) platforms have emerged as a significant innovation, offering services like lending, borrowing, and investing without the need for traditional banks. This enables financial inclusion, as people without access to conventional banking can still participate in the financial ecosystem using just an internet connection.

Supply Chain Management

In supply chain management, Blockchain ensures transparency and traceability from the origin of a product to its final destination. For instance, a food company can use Blockchain to track the journey of a product from the farm to the store shelf, ensuring quality and safety. Blockchain can pinpoint the source quickly if a contamination issue arises, reducing potential harm and costs. Companies like Walmart and IBM are already using Blockchain to manage and track supply chains, proving its effectiveness in preventing fraud and ensuring product authenticity.

Healthcare

The healthcare industry faces challenges like data breaches, inefficiencies, and fragmented patient records. Blockchain offers a solution that securely stores patient data in a decentralized system. This ensures that only authorized parties can access the information, protecting patient privacy. Moreover, Blockchain facilitates seamless sharing of medical records among healthcare providers, improving coordination and reducing errors. For example, a doctor treating a patient can instantly access their medical history on the Blockchain, avoiding duplicate tests or conflicting treatments. Blockchain also enhances the management of drug supply chains, ensuring that counterfeit medications are kept out of circulation.

Real Estate

Blockchain simplifies real estate transactions, which are often lengthy and complex. Traditionally, buying or selling a property involves numerous intermediaries, such as agents, lawyers, and banks, leading to higher costs and delays. With Blockchain, property ownership records can be securely stored, allowing faster and more transparent transactions. Smart contracts, which automatically execute agreements when conditions are met, eliminate the need for manual paperwork. This reduces fraud, speeds up the process, and lowers transaction costs. Countries like Sweden and the UAE are exploring blockchain-based land registries to modernize their real estate sectors.

Voting Systems

Trust in electoral systems is crucial for democracy, but traditional voting methods are often vulnerable to fraud, manipulation, and errors. Blockchain-based voting systems address these issues by providing a transparent and tamper-proof election platform. Each vote is recorded as a transaction on the Blockchain, making it impossible to alter without detection. Voters can verify that their votes were counted correctly, ensuring confidence. Governments and organizations worldwide are experimenting with blockchain voting to improve election integrity and boost participation by enabling secure online voting.

Intellectual Property and Copyrights

Protecting intellectual property (IP) rights is a significant challenge for artists, musicians, and creators. Blockchain offers a way to establish clear ownership of creative works through immutable records. By registering their creations on the Blockchain, creators can prove ownership and track the usage of their work. Smart contracts can automatically distribute royalties when their content is sold or used, ensuring fair compensation. This technology empowers creators by reducing reliance on third parties and combating piracy. Platforms like Audius and Verisart leverage Blockchain to support artists and protect their rights.

Benefits of Blockchain

The growing popularity of Blockchain is due to its numerous advantages:

Transparency

Blockchain technology promotes transparency by making all transactions visible to participants on the network. This level of openness builds trust among users because everyone can verify the data themselves. For example, Blockchain allows companies to track products from manufacturing to delivery in supply chain management. Customers can also access this information, ensuring that claims about product origins or sustainability are accurate.

Security

Blockchain’s security is one of its most praised features. The technology uses advanced cryptographic methods to secure data, making it nearly impossible for hackers to alter or steal information. Additionally, the decentralized nature of Blockchain ensures that even if one node is compromised, the rest of the network remains secure. Blockchain is ideal for storing sensitive information such as financial transactions, healthcare records, or identity details.

Efficiency

Traditional systems often involve intermediaries verifying and processing transactions, leading to delays and higher costs. Blockchain eliminates these intermediaries by enabling direct peer-to-peer interactions. Smart contracts—self-executing agreements coded into the Blockchain—enhance efficiency by automating processes. This means tasks like transferring property ownership or executing a trade can happen faster and with fewer errors.

Immutability

One of the key features of Blockchain is its immutability. Once data is recorded on the Blockchain, it cannot be altered or deleted. This ensures the integrity of records and reduces the risk of fraud. For example, in financial auditing, Blockchain provides an unchangeable record of transactions, making it easier to detect discrepancies and maintain trust.

Decentralization

Decentralization is at the heart of blockchain technology. Unlike traditional systems controlled by a central authority, Blockchain operates on a distributed network of nodes. This removes single points of failure and reduces the risk of system-wide outages. Decentralization also empowers users by giving them control over their data and transactions, fostering a sense of ownership and participation in the system.

Challenges of Blockchain

Despite its advantages, blockchain technology faces several challenges that must be addressed:

Scalability

One of the major hurdles for blockchain technology is scalability. As more users join a blockchain network, the system can become slower and require more transaction resources. For example, Bitcoin and Ethereum have faced issues where transaction speeds dropped and fees increased during high demand. This is because every transaction needs to be validated and recorded by multiple nodes, which takes time and computing power. To overcome this, solutions like sharding and layer-2 scaling are being developed. Sharding splits the Blockchain into smaller parts, allowing nodes to process only specific segments instead of the entire chain. Layer-2 solutions, such as the Lightning Network, handle transactions off-chain and later add them to the Blockchain, easing the burden on the main network.

Energy Consumption

Another significant challenge is the high energy consumption associated with some blockchain networks. Proof of Work (PoW), the consensus mechanism used by Bitcoin, requires miners to solve complex mathematical problems to validate transactions. This process consumes vast amounts of electricity, often comparable to the energy usage of entire countries. This has raised concerns about the environmental impact of blockchain technology. To address this, many networks are transitioning to more energy-efficient mechanisms like Proof of Stake (PoS), where validators are chosen based on the amount of cryptocurrency they hold and are willing to “stake.” PoS significantly reduces energy usage while maintaining network security.

Regulatory Issues

The regulatory landscape for Blockchain and cryptocurrencies remains unclear in many parts of the world. Governments are still figuring out how to classify and regulate blockchain-based assets. For example, some countries view cryptocurrencies as financial assets, while others classify them as commodities or currencies. This lack of consistency creates uncertainty for businesses and investors, discouraging wider adoption. Furthermore, concerns about money laundering, tax evasion, and fraud have led to stricter regulations in some regions, potentially stifling innovation. A global effort to establish clear and fair regulations is need to create a stable environment for blockchain technology to thrive.

Interoperability

Interoperability, or the ability of different blockchain networks to work together, is another critical issue. Many blockchains operate in isolation, making it difficult to transfer data or assets between them. This limits the efficiency and potential applications of blockchain technology. For instance, a healthcare blockchain may store patient records, while a supply chain blockchain tracks medication shipments. Without interoperability, integrating these systems becomes complex and inefficient. Blockchain bridges and cross-chain protocols are being develop to address this problem. These tools aim to create seamless communication between networks, unlocking new possibilities for collaboration and innovation.

Complexity

Finally, the complexity of blockchain technology poses a significant barrier to adoption. For many people and businesses, understanding how Blockchain works can be overwhelming. Cryptographic hashing, consensus mechanisms, and decentralized networks require specialized knowledge. Implementing blockchain solutions often demands significant time, resources, and expertise. This complexity makes adopting the technology challenging for small businesses or non-technical users. To make Blockchain more accessible, user-friendly platforms, educational resources, and simplified interfaces are essential. These efforts will help bridge the gap between technology and its potential users, paving the way for broader adoption.

The Future of Blockchain

The future of Blockchain looks promising, with new developments and applications emerging regularly. Here are some trends to watch:

Interoperability

Blockchain technology currently operates in silos, with many blockchains unable to share information or work together. Interoperability efforts aim to bridge this gap, allowing different blockchain networks to communicate seamlessly. This would enable users to transfer data and assets across platforms without relying on centralized intermediaries. For example, a decentralized application (DApp) on one Blockchain could integrate services from another, creating a more cohesive ecosystem. Solutions like cross-chain protocols and interoperability standards are driving this progress.

Eco-Friendly Solutions

One of the biggest criticisms of blockchain technology, especially in networks like Bitcoin, is the significant energy consumption involve in mining. To address this issue, eco-friendly solutions are being develop. For instance, Proof of Stake (PoS) replaces energy-intensive mining with a staking mechanism where participants lock up their tokens to validate transactions. Other approaches include using renewable energy for blockchain operations and creating more energy-efficient consensus algorithms. These efforts aim to make Blockchain sustainable and reduce its environmental footprint.

Decentralized Finance (DeFi)

DeFi is one of the most exciting blockchain applications, revolutionizing the financial world by removing the need for traditional banks and financial institutions. DeFi platforms allow users to lend, borrow, and trade assets directly through smart contracts. This opens up financial services to people who lack access to traditional banking. Moreover, DeFi introduces innovative concepts like yield farming and liquidity pools, enabling users to earn passive income. As the DeFi ecosystem expands, it is expect to bring financial inclusion to underserved communities worldwide.

Non-Fungible Tokens (NFTs)

NFTs have taken the world by storm, representing ownership of unique digital assets such as art, music, and collectibles. Unlike cryptocurrencies, which are interchangeable, NFTs are one-of-a-kind and stored on a blockchain to verify their authenticity and provenance. The use of NFTs extends beyond digital art—they are being apply in gaming, virtual real estate, and even ticketing systems. With continue innovation, NFTs are sets to transform how we perceive ownership and value in the digital age.

Blockchain in Government

Governments around the world are recognizing the potential of Blockchain to improve public services and increase transparency. Blockchain can simplify land registry systems by providing tamper-proof property ownership records, reducing disputes and fraud. Digital identity systems built on Blockchain can empower citizens with secure and portable identities. Blockchain-based voting systems could also enhance election integrity by ensuring transparency and preventing tampering. These initiatives demonstrate how Blockchain can bring efficiency and trust to government operations.

How Blockchain Can Change Your Life

Blockchain’s impact isn’t limit to industries; it can also benefit individuals. For instance, secure digital identities can reduce identity theft, while blockchain-based payment systems make international money transfers faster and cheaper.

Secure Digital Identities

Identity theft is a growing concern in the digital world. Blockchain offers a way to create secure, verifiable digital identities. These identities are store on the Blockchain, making them nearly impossible to forge or alter without authorization. With Blockchain, you can control who has access to your personal information and for how long, reducing the risk of data breaches and fraud.

Faster and Cheaper International Transfers

Traditional international money transfers often involve multiple intermediaries, leading to high fees and delays. Blockchain eliminates the need for intermediaries by enabling peer-to-peer transactions. This means you can send money to someone worldwide within minutes and at a fraction of the cost of traditional methods. This is especially beneficial for people in developing countries who rely on remittances from family members abroad.

Ownership of Digital Assets

With Blockchain, you can own and trade digital assets securely. Whether it’s a piece of digital art, music, or even virtual property in a game, Blockchain ensures that your ownership is record and protected. This opens up new opportunities for creators and collectors alike.

Financial Inclusion

Many people around the world don’t have access to traditional banking services. Blockchain-based financial systems, such as decentralized finance (DeFi), can give these individuals access to loans, savings, and other financial tools. All that’s need is a smartphone and an internet connection.

Transparent Charity Donations

Donating to charity is noble, but concerns about how funds are use can deter people. Blockchain can solve this by creating transparent donation systems where donors can track how their money is being spents. This increases trust and encourages more people to contribute to causes they care about.

Personal Data Control

In today’s digital world, companies often collect and use your data without your knowledge or consent. Blockchain gives you control over your data. You can decide who can access it and even monetize it by selling it directly to advertisers or researchers.

Conclusion

Blockchain technology is a game-changer that can revolutionize storing, sharing, and securing information. While it faces scalability and regulatory issues, ongoing innovations pave the way for wider adoption. Whether in finance, healthcare, or supply chain management, Blockchain’s applications are vast and transformative. As this technology continues to evolve, it’s worth keeping an eye on its developments and considering how it could shape our future.

TechWise.com is your reliable source for the latest tech news, reviews, and simple guides. We’re here to make technology easy to understand for everyone. Whether you’re a big fan of tech or just use it in your daily life, we offer helpful articles, expert advice, and practical tips to keep you updated in the fast-changing world of technology. Stay with us for the newest updates on gadgets and trends in the tech world.